What is the Heavy‑Duty Connector Market Overview – definition, scope, and significance?

The Heavy‑Duty Connector market comprises electrically conductive components designed to join power and signal lines in high‑current, rugged environments. These connectors are engineered from robust materials such as metal or high‑performance plastics and include housings, contacts, accessories, and specialized termination methods (crimp or screw). The market spans multiple end‑use sectors—including manufacturing, power generation, rail transport, oil & gas, and construction—where reliability, resistance to vibration, temperature extremes, and environmental ingress protection are critical. The market’s significance lies in its role as an enabler of industrial automation, renewable‑energy infrastructure, and transportation electrification, all of which demand durable interconnect solutions to ensure safety, uptime, and compliance with stringent standards.

What are the primary drivers, restraints, challenges, and opportunities influencing the Heavy‑Duty Connector Market?

Key drivers include the rapid expansion of renewable‑energy projects, increased electrification of rail systems, and the surge in smart‑factory initiatives that require high‑performance interconnects. Growth in oil & gas exploration and construction of large‑scale industrial facilities further fuels demand. Restraints stem from high material costs—especially for premium metals—and lengthy certification processes that can delay product rollout. Challenges involve meeting diverse regulatory requirements across regions and mitigating supply‑chain disruptions for critical components. Opportunities arise from emerging trends such as additive manufacturing of custom connector housings, integration of sensor‑based health monitoring, and the development of modular, plug‑and‑play systems that accelerate installation in remote or hazardous locations.

What are the current and emerging growth trends shaping the Heavy‑Duty Connector Market?

Current trends focus on miniaturization without sacrificing current‑carrying capacity, leading to compact yet robust designs. There is a noticeable shift toward environmentally sealed connectors that meet IP68 standards for dust and water resistance. Emerging trends include the adoption of smart connectors equipped with embedded diagnostics, the use of alloy‑based contacts that reduce resistance loss, and the rise of standardized modular platforms that simplify cross‑industry integration. Moreover, the push for circular economy practices is prompting manufacturers to explore recyclable materials and take‑back programs.

How has COVID‑19 impacted the Heavy‑Duty Connector Market and what is the recovery trajectory?

The pandemic initially disrupted manufacturing output and logistics, causing temporary demand dips in sectors such as construction and rail. However, the acceleration of automation and the fast‑track deployment of renewable‑energy infrastructure during recovery periods offset those losses. As supply chains have stabilized, the market is experiencing a robust rebound, underpinned by renewed investment in industrial digitization and infrastructure projects, positioning it on a clear upward trajectory.

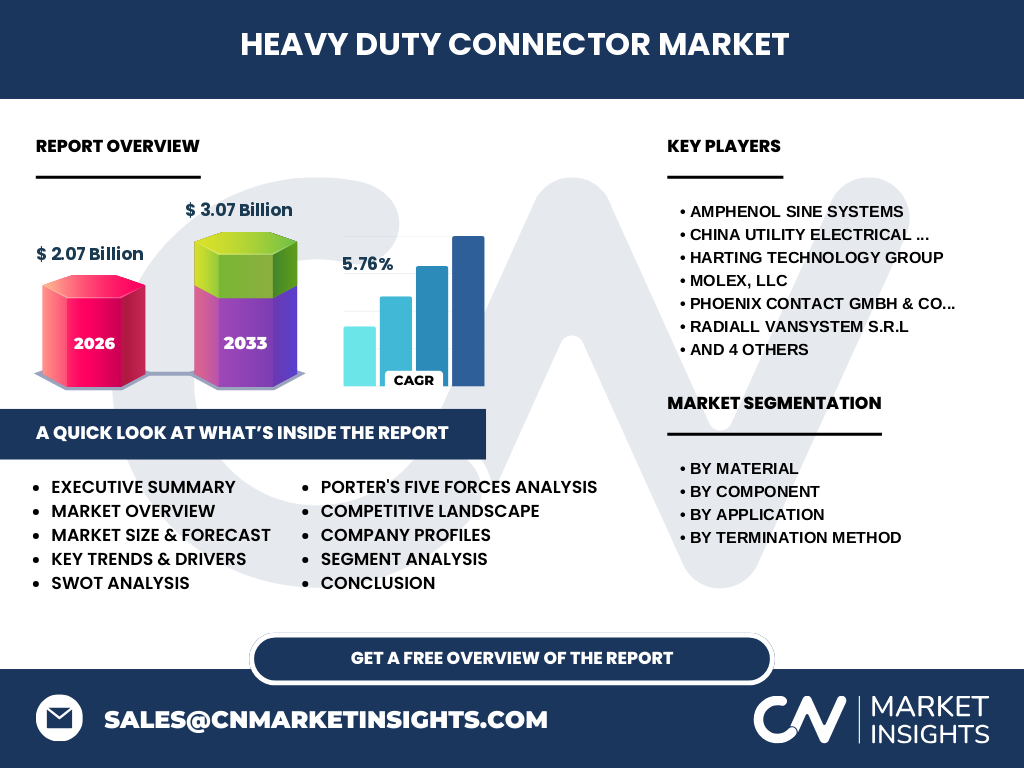

Who are the major competitors in the Heavy‑Duty Connector Market and what does the competitive landscape look like?

The market is highly competitive, featuring globally recognized firms such as Amphenol Sine Systems, HARTING Technology Group, TE Connectivity, Molex, Phoenix Contact, Smiths Interconnect, Radiall VanSystem, Weidmüller Interface, Wieland Electric, and China Utility Electrical Co., Ltd. These players compete on technology leadership, product breadth, and after‑sales service. Recent years have seen strategic consolidations, joint ventures, and acquisitions aimed at expanding portfolio coverage and geographic reach, leading to a moderately consolidated landscape dominated by a handful of large, diversified manufacturers.

What are the key findings highlighted in the Executive Summary of the Heavy‑Duty Connector Market?

The Heavy‑Duty Connector market is projected to reach 3.07 billion USD by 2033, up from 2.07 billion USD in 2026, reflecting a CAGR of 5.76 % over the forecast horizon. Growth is driven by electrification trends across rail and power sectors, expanding renewable‑energy installations, and heightened automation in manufacturing. Material innovation and smart‑connector technologies present significant upside potential. The market remains resilient despite past supply‑chain shocks, with leading players reinforcing their positions through R&D investment and regional expansion.

What is the forecast for the Heavy‑Duty Connector Market from 2025 to 2032?

Based on the provided data, the market is expected to grow from 2.07 billion USD in 2026 to 3.07 billion USD by 2033, delivering a compound annual growth rate of 5.76 %. This steady expansion suggests a consistent increase in annual revenue of roughly 140 million USD, driven by sector‑specific demand and ongoing product innovation.

How is the Heavy‑Duty Connector Market sized and shared by segment?

Segmentation by material shows two primary groups: metal and plastic connectors, each catering to different performance and cost requirements. By component, the market divides into hoods & housings, inserts & contacts, and accessories, with housings typically commanding the largest share due to their critical role in protection and mechanical integrity. Application‑wise, the market is spread across manufacturing, power, rail, oil & gas, and construction, with manufacturing and power sectors historically representing the bulk of demand. Termination methods are split between crimp and screw solutions, where crimp connectors dominate owing to their superior vibration resistance, while screw terminations retain niche relevance in retrofit and low‑volume applications.

What is the global Heavy‑Duty Connector market size and share by region?

The market exhibits a worldwide footprint, with North America, Europe, Asia‑Pacific, and Rest‑of‑World regions participating. While precise regional revenue figures are not disclosed, the presence of major OEMs and high‑growth infrastructure projects in Asia‑Pacific suggests a strong and expanding share, whereas North America and Europe maintain stable, mature demand driven by industrial automation and rail electrification. The Rest‑of‑World regions contribute incremental growth through emerging construction and oil & gas activities.

What does the regional analysis of the Heavy‑Duty Connector Market reveal?

In North America, market growth is anchored by advanced manufacturing and legacy rail networks undergoing modernization. Europe shows steady expansion fueled by stringent environmental regulations encouraging renewable‑energy projects and high‑speed rail upgrades. Asia‑Pacific is the fastest‑growing region, propelled by large‑scale infrastructure investments, rapid industrialization, and expansive power‑grid expansions. The Rest‑of‑World, encompassing Latin America, Middle East, and Africa, exhibits modest but notable growth, primarily in oil & gas exploration and new construction ventures.

Which companies lead the Heavy‑Duty Connector market and what are their strategic approaches?

Key leaders such as Amphenol Sine Systems, HARTING Technology Group, TE Connectivity, and Molex focus on broad product portfolios, extensive global distribution networks, and continuous innovation in high‑temperature alloys and smart‑connector technologies. Phoenix Contact and Weidmüller prioritize modular system integration and digital services. Radiall VanSystem and Smiths Interconnect leverage niche expertise in aerospace and defense connectors to cross‑sell heavy‑duty solutions. Wieland Electric emphasizes sustainability through recyclable metal designs, while China Utility Electrical Co., Ltd leverages cost‑effective manufacturing capabilities to capture price‑sensitive segments.

How does Porter’s Five Forces analysis apply to the Heavy‑Duty Connector Market?

Threat of new entrants is moderate; high capital requirements and stringent certification create barriers, yet emerging low‑cost manufacturers in Asia‑Pacific increase pressure. Bargaining power of suppliers is relatively high for specialty alloys and high‑purity plastics, given limited sources. Bargaining power of buyers is strong in commoditized segments, as large OEMs can negotiate volume discounts. Threat of substitutes is low because alternative interconnect technologies cannot match the current‑carrying capacity and ruggedness required. Industry rivalry is intense, driven by product differentiation, innovation cycles, and strategic acquisitions.

What are the SWOT insights for the Heavy‑Duty Connector Market?

Strengths: Established demand across critical infrastructure, high technical barriers to entry, and strong IP portfolios.

Weaknesses: Dependence on volatile raw‑material prices and long certification timelines.

Opportunities: Smart‑connector integration, additive manufacturing, and expansion into emerging markets.

Threats: Global supply‑chain disruptions, aggressive price competition from low‑cost producers, and evolving regulatory standards requiring redesign.

What does the value chain of the Heavy‑Duty Connector Market look like?

The value chain begins with raw‑material sourcing (copper, aluminum, engineered plastics), followed by component engineering, precision molding or machining, contact plating, assembly of housings and contacts, testing (electrical, environmental), and final distribution through OEM channels or direct sales. After‑sales services, including maintenance kits and technical support, close the loop, adding recurring revenue streams for manufacturers.

What key investment insights can be derived for the Heavy‑Duty Connector Market?

Investors should prioritize companies with diversified material portfolios and proven capabilities in smart‑connector technologies, as these are poised for premium pricing. Strategic focus on firms expanding in the Asia‑Pacific region can capture higher growth rates. Partnerships with renewable‑energy project developers provide a pipeline of long‑term contracts. Additionally, firms that own in‑house plating and testing facilities mitigate supply‑chain risks and enhance margins.

What conclusions can be drawn about the Heavy‑Duty Connector Market?

The Heavy‑Duty Connector market is on a clear growth trajectory, forecast to reach 3.07 billion USD by 2033 at a 5.76 % CAGR. Its resilience stems from essential roles in electrification, automation, and infrastructure resilience. While material costs and regulatory complexity pose challenges, innovation in smart diagnostics and modular designs present substantial upside. Leading vendors are consolidating capabilities to sustain competitive advantage, making the sector attractive for long‑term investors.

What research methodology was employed for this market study?

The analysis combined primary interviews with industry experts, OEM engineers, and supply‑chain managers, alongside secondary data from company reports, trade publications, and governmental databases. Market sizing utilized a top‑down approach anchored to the 2026 base figure of 2.07 billion USD, with growth extrapolated using the provided 5.76 % CAGR. Segmentation assumptions were validated through cross‑referencing product catalogs and procurement data.

What is the scope of this research, including coverage and limitations?

The study covers global Heavy‑Duty Connector market dynamics, segmented by material, component, application, and termination method, with regional breakdowns for major geographies. It focuses on the period 2025–2033 and incorporates the latest competitive moves by leading firms. Limitations include the reliance on publicly available financial disclosures and the exclusion of confidential contractual terms that may affect specific pricing dynamics.

Which key companies and recent developments define the Heavy‑Duty Connector Market?

Amphenol Sine Systems recently launched a high‑temperature cermet contact line targeting rail electrification. HARTING announced a strategic partnership with a leading renewable‑energy EPC to supply rugged connectors for offshore wind farms. TE Connectivity introduced a smart‑connector platform with integrated temperature sensors for predictive maintenance. Molex expanded its plastic‑housing portfolio to address cost‑sensitive construction projects. Phoenix Contact unveiled a modular housing system enabling rapid field reconfiguration. These developments underscore the market’s focus on innovation, sustainability, and strategic collaborations.